A Guide To Cell Phone Contracts and Blacklisting or Low Credit Score-Cards

Phonefinder is all about cell phones. Be it cell phone contracts, repairs, news, reviews, or accessories. We're especially proud of our cell phone contract comparison tool. There are up to 5000 unique deals available from Vodacom, MTN, Cell C, and Telkom.

However, applying for a cell phone contract isn't as easy as it used to be.

You may be one of the 80% of South Africans who were declined for a contract this year. You pay your bills, have a job – so why were you declined? It feels unfair and definitely frustrating.

Why then were you declined a cell phone contract?

It often comes down to being “blacklisted”. A cell phone contract is part subscription, part loan. If your credit history is poor, you can't get the loan. That’s the tough truth.

While we can’t change your score, we can help you understand what’s happening, why it happens, and what to do next.

I have a low ITC score but I am not blacklisted

For most networks, a low score is as risky as being blacklisted. Even if you have a stable job, a low score can keep you from getting a contract. MTN, Cell C, Vodacom, and Telkom all use their own secret scorecards – and they’re getting harder to pass.

Fortunately, some providers are more flexible. They operate with lower score requirements, so your chances improve with them.

What does it mean to be "blacklisted"?

There’s no official "blacklist". The term simply refers to a negative credit score – and that can stop you from getting credit.

What information is used to form a blacklist judgement?

Payment defaults, judgments, sequestrations, or administration orders.

What can be done to prevent a bad credit record?

Pay your bills on time and in full. That’s the most important step.

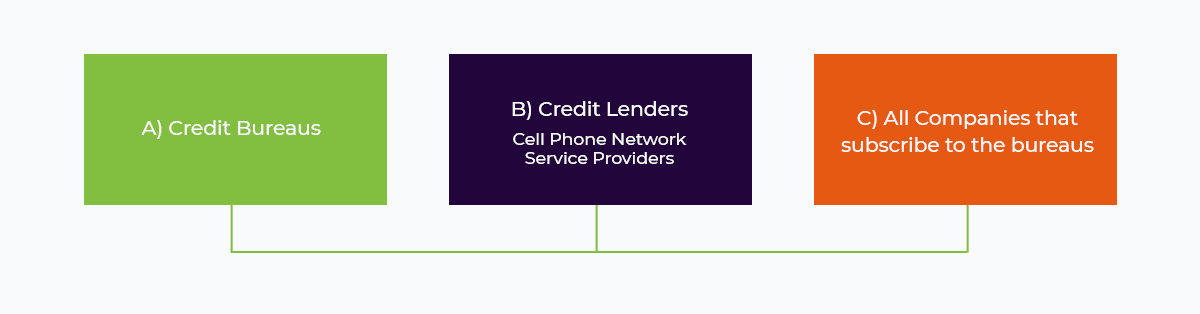

Becoming blacklisted: how it works

A) Credit bureaus: TransUnion ITC and Experian

B) Credit providers (e.g. retailers, networks, banks)

C) Subscribers to the bureaus

If you don’t pay C, your info goes to A, so B can use it to make lending decisions.

How long will my credit records be tainted?

Defaults and judgments stay on your report for 5 years – even after repayment.

Can I Clear My Name?

Yes, but it takes effort. You’ll need a lawyer, proof of payment, and a magistrate to clear the listing. Once done, all bureaus must update their records.

Update: Since March 13, 2015, thanks to the National Credit Amendment Act, adverse listings fall off after one year if paid. No lawyer needed for that anymore.

There is no shame in being blacklisted

You might owe as little as R500 to get blacklisted – maybe because an invoice never arrived. It happens. And it’s fixable.

Check your credit status for free

Want to speed up your contract approval? First, check your credit. You’re entitled to one free credit report per year:

Some handy legal terms

The following terms help make sense of your credit report:

Delinquent Classification: You pay late but you do pay.

Default: You’ve failed to pay per your agreement.

Judgment: A legal order following a summons. Must be cleared in court to be removed.

Administration Order: Available if your total debt is under R50,000. Pay monthly via an administrator until settled.

Sequestration: Court-declared bankruptcy. You won’t be able to access credit for up to 10 years.